Table Of Contents

Fixed Capital Method Fluctuating Capital Method | Methods Of Capital Accounts Explanation

Learn Everything About Fixed Capital Method Fluctuating Capital Method Methods of capital accounts :

In absence of any provision in a partnership deed , Indian Partnership Act 1932 , says that all partner should contribute equal amount of capital.

But partners may put a special clause in their Partnership Deed of having unequal capital. It means, as per provisions of the partnership Deed, the partners may have unequal capitals. Because it is possible, that an active or very experienced partner may provide less amount of capital compared with others, a Nominal Partner not provides capital. Therefore to have clear amount of capital of each partner year after year, the partnership firm may adopt any of the following 2 methods for maintaining Partners Capital Account –

- Fluctuating Capital Method / Floating Capital Method .

- Fixed Capital Method .

Fluctuating Capital Method :

Under this method only a capital account for each partner is maintained. We have to record various adjustments like drawings, interest on capital, interest on drawings, net profit or loss etc.

If such adjustments like drawings, interest on capital, interest on drawings, salary or commission to partners, share of their net profit / loss etc. are recorded in their Capital A/c, due to such various adjustments amount of their capital changes. In such a method, the amount of opening capital and closing capital will be different due to such adjustments.

Such a Capital method in which an amount of capital of partners changes due to various adjustments passed in the capital accounts is said to be a fluctuating capital method or floating capital method .

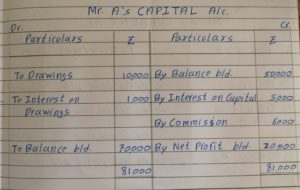

For example :

In the above capital account in addition to the amount of opening capital Rs 50,000, the various adjustments are recorded in it. As a result of all such adjustments, the amount of opening capital increased to Rs 70,000 at the end of year. It means the amount of capital has beeen changed. Therefore this method is said to be a Fluctuating Capital Method .

Fixed Capital Method :

When the Partnership firm wants to maintain amount of capital fixed year after year, it has to adopt fixed capital method . If the firm intends that the amount of capital should not affect the basic amount of capital, it has to adopt the fixed capital method .

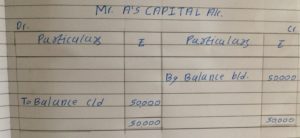

In such a case, the firm has to open 2 accounts for each partner –

- Partners Capital Account &

- Partners Current Account

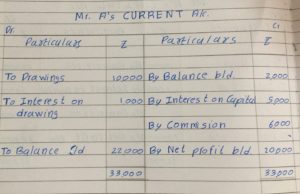

In such a method all the adjustments like drawings, interest on capital, interest on drawings, salary / commission to partner, net profit etc. are –

- Not recorded in Partners Capital Account

- But such adjustments are recorded in a special account called as Partners Current Account .

As all such adjustments are recorded in Partners Current Account , the balance of capital, in Capital Account remains fixed year after year. Therefore this method of maintaining capital account is said to be a Fixed Capital Method .

The method of maintaining capital accounts , in which the amount of capital remains fixed year after year is called Fixed Capital Method .

Example –

• If the additional capital is introduced during the year, it is recorded in Partners Capital Account. It is not recommended in Partners Capital Account. Due to such a transition that particular year, balance on capital account will change. It means original principal amount of capital increases due to additions.

• Similarly if the am amount of capital is withdrawn, it is also recorded in the Partners Capital Account due to such drawings the original principal capital decreases. But drawings are out of profits, then they appears in Partners Current Account and not in capital account. Normally drawings are assumed out of profits.

• The Partners Current Account may show either a debit balance or a credit balance –

1. The debit balance of partners current account appears on asset side of balance sheet.

2. The credit balance of partners Current Account appears on liabilities side of balance sheet.